Buying your first home is one of life’s biggest milestones, an exciting, empowering, and sometimes a little overwhelming . With rising house prices, changing mortgage rules, and a competitive property market, it’s no surprise that many first‑time buyers feel unsure about where to begin.

This guide breaks everything down in a clear, friendly way so you can move forward with confidence. Whether you’re saving for a deposit, comparing mortgage options, or preparing to make an offer, you’ll find practical advice to help you take the next step on your home buying journey.

Who Counts as a First‑Time Buyer?

A first‑time buyer is someone who has never owned a property before, anywhere in the world. This status comes with major advantages, including:

– Lower stamp duty (or none at all)

– Access to first‑time buyer mortgage deals

– Government schemes designed to help you onto the ladder

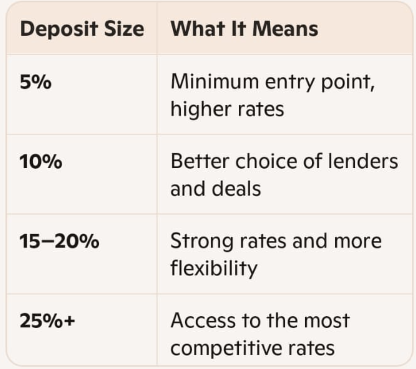

How Much Deposit Do You Need?

Most lenders require a minimum 5% deposit, but the more you can put down, the better your mortgage rate is likely to be. Here’s a quick breakdown:

How Lenders Assess Your Affordability

Mortgage lenders look at:

– Your income

– Your outgoings and credit commitments

– Your credit history

– Your deposit size

– Your job type and stability

They typically lend 4–4.5 times your annual income, though some lenders may offer more in certain circumstances.

Understanding Mortgage Types

Fixed-Rate Mortgage

Your interest rate remains constant for a specific duration (typically 2, 3, 5, or 10 years).

Predictable payments: Your monthly outgoings stay the same regardless of market changes.

Rate protection: You are shielded from any increases in the Bank of England base rate.

Variable or Tracker Mortgage

Your interest rate fluctuates, usually in direct alignment with the Bank of England base rate.

Potential savings: These can be significantly cheaper if interest rates fall.

Flexibility: Often comes with more flexible terms and lower early repayment charges.

Guarantor or Family-Assisted Mortgages

These are designed for buyers with smaller deposits or lower annual incomes.

Boosted affordability: Leveraging family support can help you qualify for a larger loan.

Market entry: Allows you to purchase a property sooner than you might on your own.

Expert Tip: A mortgage broker can help you compare specific deals across the market and determine which of these options best suits your unique financial situation.

How Lenders Assess Your Affordability

1. Check your credit score

2. Save your deposit

3. Get an Agreement in Principle (AIP)

4. Start viewing properties

5. Make an offer

6. Apply for your mortgage

7. Instruct a solicitor

8. Get a survey

9. Exchange contracts

10. Complete and collect your keys

Each step has its own timeline, but a our team can guide you through the process smoothly.